Giggle Finance Requirements: Who Qualifies and Who Gets Denied?

- Jason Feimster

- 1 day ago

- 11 min read

Giggle Finance says it works with freelancers, gig workers, independent contractors, and small business owners—but approval is not magic. Here’s what they actually look for before you apply and get your hopes drop-kicked.

Fast funding sounds great until the application asks for bank activity, business income, deposits, and proof that your hustle is more than a financial fever dream with a DoorDash bag.

If you're researching Giggle Finance requirements, the real question is not just “Can I apply?” It's:

“Do I actually look fundable before I hand over my information and emotionally pre-spend the money?”

Giggle Finance says it works with freelancers, gig workers, independent contractors, 1099 workers, self-employed professionals, and small business owners. That sounds broad. But broad does not mean automatic. Approval is not magic. It is usually based on your income activity, bank account history, business or 1099 deposits, repayment capacity, and whether your profile fits what the funding provider is willing to take on.

Translation: your hustle may qualify. Your chaos may not.

TL;DR: What Are the Basic Giggle Finance Requirements?

Giggle Finance generally looks for applicants with 1099 or small business income, at least three months of activity, an eligible bank account with online access, and enough revenue or deposits to show repayment ability. Credit score may not be the main factor, but bank history, deposits, negative balances, overdrafts, and account stability can still matter.

Giggle Finance Requirements At a Glance

Category | What to Know |

|---|---|

Best for | Gig workers, freelancers, independent contractors, app-based workers, and small business owners with regular deposits |

Not ideal for | W-2-only employees, inconsistent earners, or applicants with unstable bank activity |

Funding type | Revenue-based advance / cash-flow-based funding |

Typical borrower profile | DoorDash drivers, Uber/Lyft drivers, freelancers, consultants, mobile service workers, small operators |

Time in business | Giggle publicly references at least three months of 1099 or business income |

Income requirement | Public pages reference minimum revenue/deposit thresholds; verify current terms before applying |

Bank account required? | Yes, Giggle says applicants need a bank account with online access and business or 1099 deposits |

Credit score factor | Giggle says eligibility is based more on banking history than past credit |

Biggest denial risk | Weak deposits, W-2-only income, overdrafts, negative balances, chargebacks, or unstable cash flow |

Best next step | Review your bank activity before applying and make sure your income story is clean |

What Is Giggle Finance?

Giggle Finance is a fast-funding platform built for independent workers and small business operators who may not fit traditional bank underwriting.

Traditional banks usually want clean tax returns, strong credit, formal business financials, time in business, and documentation that makes your life look like a corporate brochure.

Gig workers usually live in a different reality.

Maybe your income comes from Uber, Lyft, DoorDash, Instacart, Fiverr, Upwork, TaskRabbit, Airbnb, Etsy, Shopify, or freelance clients. You might have real revenue but messy paperwork. You might have deposits every week but no traditional employer. You might be making money, but on paper, a bank looks at you like you’re a raccoon wearing a LinkedIn badge.

Giggle Finance appears designed for that gap. Instead of focusing only on credit score, it looks more closely at revenue, deposits, business activity, and bank history. That can help people who earn money but do not look clean in traditional underwriting. But it also means your bank account becomes the story.

If that story is ugly, the answer may still be no.

How Does Giggle Finance Work?

The process is usually simple:

Apply online.

Provide personal, business, or gig-work information.

Connect or verify your bank account.

Giggle reviews your income and bank activity.

You receive a decision or offer if eligible.

You review the terms.

You accept or decline.

Repayment follows the agreement.

The key step is the bank connection. Giggle says applicants need to connect a bank account so income and account activity can be reviewed.

That does not mean approval is guaranteed. It means your bank account gets pulled into the underwriting spotlight like a defendant on a courtroom drama.

Before accepting anything, confirm:

How much you receive

How much you repay

When repayments happen

Whether payments are fixed, weekly, or tied to revenue

Whether there are fees

Whether early payoff changes the cost

What happens if your income drops

Do not accept funding until you understand the repayment amount, schedule, fees, and total cost.

Giggle Finance Qualification Requirements: What They May Look At

Giggle Finance requirements are mostly about whether your income and bank activity show that you can reasonably repay the advance.

Here are the main qualification categories.

1. 1099 or Small Business Income

Giggle is not primarily built for traditional W-2-only employees. It is positioned for:

1099 workers

Independent contractors

Freelancers

App-based gig workers

Small business owners

Self-employed professionals

Consultants

Mobile service providers

Marketplace sellers

If your income comes only from a W-2 job, you may not qualify.

If you have both W-2 income and 1099 or business income, you may still have a shot, but the business or gig income likely needs to show up clearly.

Practical Takeaway

Giggle wants to see business-style income, not just a paycheck from an employer.

2. Time in Business or Gig Activity

Giggle publicly references at least three months of business or 1099 income.

That matters because one good week does not prove repayment capacity. A sudden $900 payout from one chaotic weekend of rideshare work is nice, but underwriting wants a pattern. Lenders and funding providers generally prefer consistency over one-time spikes.

You do not need to be a 10-year business veteran with a mahogany desk and a CFO named Brent. But you probably do need enough history to prove the income is real.

Practical Takeaway

If you just started gig work last Tuesday, wait until you have more deposit history before applying.

3. Income Requirements and Deposit Activity

This is where borrowers need to pay close attention.

Giggle’s public pages have referenced different income or deposit thresholds, including monthly revenue requirements and bank-account deposit expectations. That means you should verify the current requirement directly before applying.

The practical issue is simple: Giggle wants to know whether money is regularly coming in.

Approval may depend on:

Average monthly revenue

Weekly deposits

Number of deposits in the last month

Whether the deposits look like business or 1099 income

Whether your cash flow is stable enough to support repayment

Whether your account balance regularly goes negative

A gig worker making $4,000 per month with consistent weekly deposits may look stronger than someone who made $5,000 once and then had three weeks of account tumbleweeds.

Practical Takeaway

Consistency beats drama. Bank activity should show real earning rhythm, not financial jump scares.

4. Bank Account Requirements

Giggle says applicants need a bank account with online access and business or 1099 deposits. The account may need to be connected through a third-party processor so income and activity can be reviewed.

This is not just a technical step. It is part of the approval process.

They may review:

Deposit frequency

Deposit sources

Average daily balance

Negative balances

Overdrafts

Chargebacks

Recent account activity

Business or 1099 income signals

If your bank account is a flaming circus of overdrafts, returned payments, and “available balance: emotional damage,” approval odds may drop.

Practical Takeaway

Before applying, clean up your bank account as much as possible. The bank connection is not decoration. It is underwriting.

5. Credit Score Requirements

Giggle says credit score is not the main factor and that eligibility is based more on banking history than past credit.

That can be useful for borrowers with bad credit, thin credit, or old financial bruises. But “credit score is not the main factor” does not mean “nothing matters.”

Revenue-based funders may still care about whether your bank activity shows repayment capacity. A low credit score may not automatically block you, but weak deposits, negative balances, or unstable cash flow can still create problems.

This is the trap with “no credit check” or “credit score not required” messaging. People hear “they don’t care about credit” and assume approval is automatic.

Nope.

They may not grade the same homework as a bank, but they are still grading something.

Practical Takeaway

Bad credit may not kill your application, but bad cash flow still can.

Who Is Most Likely to Qualify for Giggle Finance?

You may be a better fit if you:

Have at least three months of 1099 or business income

Receive regular gig, freelance, or small business deposits

Have a bank account with online access

Avoid frequent overdrafts or negative balances

Have enough deposits to support repayment

Need short-term funding for a business or income-producing purpose

Understand that repayment will affect future cash flow

Examples of applicants who may fit:

DoorDash driver with steady weekly payouts

Uber or Lyft driver with consistent rideshare income

Freelancer with regular client payments

Barber, mobile detailer, or mobile service provider with recurring revenue

Etsy, Shopify, or eBay seller with marketplace deposits

Consultant with ongoing client income

Independent contractor with 1099 deposits

Who Gets Denied by Giggle Finance?

Giggle does not publish a universal denial checklist, and approval decisions can vary. But based on the stated requirements and how cash-flow-based funding generally works, these profiles may struggle.

W-2-only employees

Giggle specifically says W-2-only workers do not qualify. If you only have traditional employee wages and no business or 1099 income, this may not be the right product.

Too little income history

If you have not been earning business or 1099 income long enough, your application may be too thin.

Weak or inconsistent deposits

If deposits are random, infrequent, or too low to support repayment, approval odds can suffer.

Bank account problems

Overdrafts, negative balances, chargebacks, returned payments, and unstable average balances can all make the file look risky.

No eligible bank account connection

If you cannot connect the right account or the account does not show your gig or business income, the application may stall or fail.

Using the money for panic spending

This may not be a formal denial reason, but it is a personal red flag. If the funding does not help you earn more, stabilize income, or fix an income-producing problem, slow down.

Practical Takeaway

Getting denied does not always mean you are broke. Sometimes it means your bank activity does not yet tell a clean enough story.

How to Improve Your Giggle Finance Approval Odds

You cannot control every underwriting factor. But you can make your profile less chaotic before applying.

Start here:

Use one primary bank account for gig or business deposits

Avoid overdrafts before applying

Let deposits build consistently

Keep your account balance positive

Separate personal spending from business income where possible

Make sure your platform payouts are visible

Avoid applying immediately after a bad bank-account week

Review your repayment capacity before accepting an offer

The goal is not to fake anything.

Do not lie.

Do not manipulate documents.

Do not play spreadsheet cosplay with money you do not have.

The goal is to make your income easier to verify.

Funding providers like clean stories.

Give them one.

Giggle Finance Requirements vs. Traditional Bank Requirements

Requirement | Giggle Finance-style funding | Traditional bank loan |

|---|---|---|

Credit score | May not be the main factor | Often very important |

Tax returns | May not be the main focus | Often required |

Bank activity | Very important | Important but not always enough |

Time in business | Publicly references shorter history requirements | Often 1–2+ years |

Collateral | Usually not the main driver | May be required |

Speed | Built for fast decisions | Often slower |

Repayment risk | Can hit cash flow quickly | Usually structured over longer terms |

Best fit | Fast short-term needs | Larger, lower-cost, longer-term funding |

Traditional banks usually reward clean paperwork and strong credit. Revenue-based funding usually rewards visible cash flow. Neither is “better” in every situation. They solve different problems.

A bank loan may be cheaper but slower and harder to qualify for.

Fast funding may be easier but can cost more and affect weekly cash flow.

Choose based on the problem, not the dopamine hit of seeing “approved.”

Before You Apply for Giggle Finance, Check This

Use this checklist before you apply:

Do I have 1099, freelance, gig, or small business income?

Have I been earning that income for at least three months?

Does my bank account show regular deposits?

Do I know my average monthly revenue?

Do I have recent overdrafts or negative balances?

Can I connect the bank account where my income lands?

Am I comfortable linking my account through a third-party processor?

Do I know how much I can afford to repay weekly?

Am I using the money for an income-producing need?

Have I compared other options before accepting?

Do I understand the total repayment amount?

Do I know what happens if my income drops?

If you cannot answer these cleanly, pause before applying. Your future self may appreciate not being ambushed by your current self’s panic-clicking.

Giggle Finance Alternatives to Consider

If you do not meet the requirements, or if the repayment terms do not fit, compare other options before giving up.

Option | Best for | Speed | Flexibility | Risk | Main Caution |

|---|---|---|---|---|---|

Giggle Finance | Gig workers and self-employed borrowers with regular deposits | Fast | More flexible than banks | Medium to high | Verify total repayment and bank requirements |

Cash advance apps | Small personal gaps | Fast | Often flexible | Medium | Limits may be low and fees/tips can add up |

Business line of credit | Repeat working capital needs | Moderate | Varies | Medium | Harder to qualify for weak-credit borrowers |

Revenue-based financing | Businesses with steady deposits | Moderate to fast | Flexible | Medium to high | Repayment can pressure cash flow |

Local credit union loan | Lower-cost personal or small business needs | Slower | Varies | Lower to medium | May require stronger credit or documentation |

Business funding marketplace | Comparing multiple offers | Moderate | Varies | Varies | Avoid accepting the first offer without comparing |

The move is not “Giggle or nothing.”

The move is:

Know what you qualify for, understand repayment, and choose the funding option that solves the actual problem without putting next week’s income in a chokehold.

Reality Check: Approval Is Not the Same as Affordability

Getting approved feels good. It can feel like the financial universe finally stopped throwing chairs at you.

But approval does not mean the funding is smart.

A good funding decision should do one of three things:

Help you earn income

Protect your ability to work

Bridge a temporary cash-flow gap with a clear repayment plan

A risky funding decision usually does this:

Covers recurring shortfalls

Replaces budgeting with borrowed money

Pays off another advance

Creates another repayment problem next week

Lets panic pretend to be strategy

If the money helps fix the car that earns the money, that may be a useful bridge.

If the money only helps you survive until the next shortfall, pause before your future deposits become a piñata.

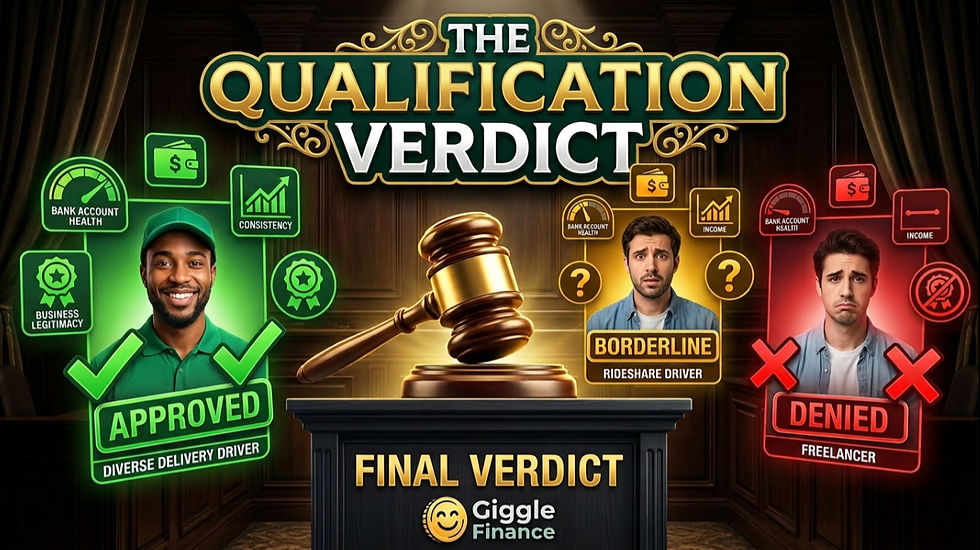

Final Verdict: Who Qualifies for Giggle Finance?

Giggle Finance may be worth considering if you are a gig worker, freelancer, independent contractor, self-employed professional, or small business owner with regular 1099 or business income, at least a few months of activity, and a bank account that clearly shows your deposits.

You should be cautious if your income is inconsistent, your account has recent overdrafts or negative balances, you are W-2 only, or you do not understand how repayment will affect your cash flow.

The cleanest answer:

Giggle Finance requirements are less about perfect credit and more about proving that your income is real, consistent, and strong enough to support repayment.

Before applying, review your bank activity, know your income, understand the repayment terms, and compare alternatives.

FAQ: Giggle Finance Requirements

What are the basic Giggle Finance requirements?

Giggle Finance generally looks for applicants with 1099 or small business income, at least a few months of activity, and a bank account that shows business or gig-work deposits. Public pages reference income and deposit requirements, but borrowers should verify current terms directly before applying.

Does Giggle Finance require a credit score?

Giggle says credit score is not the main factor and that eligibility is based more on banking history than past credit. That does not mean everyone qualifies. Bank deposits, cash flow, negative balances, overdrafts, and repayment capacity may still affect approval.

Does Giggle Finance require a bank account?

Yes. Giggle says applicants need a bank account with online access and business or 1099 deposits. The bank account may need to be securely connected through a third-party processor so income and account activity can be reviewed.

How much income do you need for Giggle Finance?

Giggle’s public pages have referenced minimum revenue or deposit requirements, including monthly revenue and recent deposit expectations. Because requirements can change or vary by product, applicants should verify the current income threshold before applying.

Can W-2 employees qualify for Giggle Finance?

Giggle says W-2-only workers do not qualify. The product is designed for 1099 workers, independent contractors, freelancers, self-employed professionals, and small business owners. If you have both W-2 and business or 1099 income, your business income may still matter.

Why would Giggle Finance deny an application?

Possible denial reasons may include W-2-only income, not enough business or 1099 history, weak deposits, unstable bank activity, overdrafts, negative balances, chargebacks, or an inability to connect the right bank account. Approval depends on the applicant’s full profile and current underwriting rules.

Is Giggle Finance good for DoorDash or Uber drivers?

Giggle Finance may fit some DoorDash, Uber, Lyft, Instacart, and app-based workers if they have regular deposits and meet the stated requirements. Drivers should review total repayment, bank connection terms, and whether the funding helps protect income before accepting an offer.

Comments