Wix Seller Financing: Funding Options for Wix Stores

- Jason Feimster

- Apr 25

- 8 min read

You can't ship what you can't stock. And you can't stock what you can't fund.

Your Wix store is converting. Orders are rolling in. But your supplier wants 50% upfront for the next container, Facebook wants its ad budget tomorrow, and your bank account is frozen between last month's expenses and next week's payout. You're not broke—you're just cash-trapped. And that gap is costing you sales every single day.

Why Banks Fail Here

Traditional lenders don't speak eCommerce. They see "online business" and immediately ask for two years of tax returns, personal collateral, and a 680+ credit score. Then they take 45 days to say no.

Here's why the legacy system doesn't work for Wix sellers:

They don't understand rolling inventory cycles — Banks want steady W-2 income, not seasonal spikes and SKU gambles.

Payout delays confuse underwriters — Wix Payments batches deposits; banks see "inconsistent revenue" and panic.

They require collateral you don't own yet — Your best asset is inventory you haven't bought. Good luck explaining that to a loan officer.

Speed kills deals — By the time a term loan clears, your supplier sold out and your competitor launched the same product.

Profit ≠ cash — You can be profitable on paper and still miss payroll because capital is tied up in transit or ad spend.

Actionable Plays

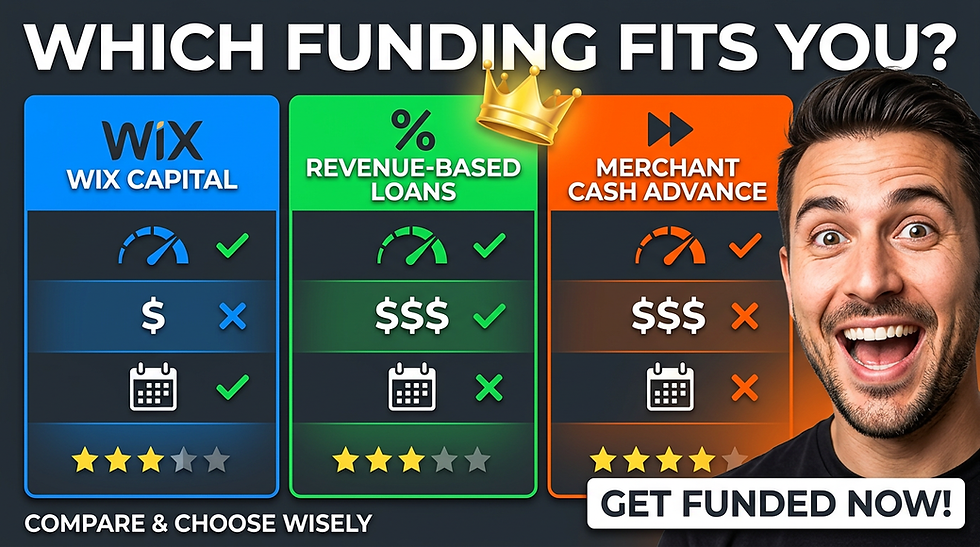

Play 1: Wix Capital — The House Money Option

What it is:

Wix's native funding tool. They front you cash based on your store's sales velocity, then auto-deduct a fixed percentage from each sale until repaid.

When it works best:

You're doing consistent monthly revenue ($5K+)

You need inventory or ad spend fast

You don't want to juggle external lenders

Your Wix sales data is clean and growing

Common pitfalls:

The percentage deduction eats into margin during slow months. If you have a seasonal dip, you're still paying the same rate per sale — which can choke cash flow when you need it most.

What you need to qualify:

Active Wix eCommerce plan

Payment processing through Wix Payments

At least 4 months of transaction history

No red flags (chargebacks, suspended account)

Operator checklist:

[ ] Log into Wix dashboard → check Capital eligibility

[ ] Review your repayment rate (usually 10–20% per transaction)

[ ] Model it against your worst-case monthly sales — can you survive the draw?

[ ] Set aside 15% buffer cash before accepting the advance

[ ] Track repayment in a separate spreadsheet weekly

Play 2: Revenue-Based Financing (RBF) — The Growth Lever

What it is:

Lenders (Clearco, Uncapped, Capchase) advance capital and take a percentage of daily or weekly revenue until repaid + fee. No fixed monthly payment. Scales with sales.

When it works best:

You're scaling paid ads or influencer campaigns

Revenue is unpredictable month-to-month

You can't stomach a traditional term loan

You need $10K–$500K range

Common pitfalls:

RBF can feel "cheap" because there's no APR listed — but total payback can hit 1.3–1.5x what you borrowed. Do the math. And if sales explode, you pay back faster but at a higher effective cost.

What you need to qualify:

$10K+ monthly revenue (some require $25K+)

Connect bank account + ad accounts (Facebook, Google)

6–12 months operating history

Positive unit economics (prove you're not burning cash per sale)

Operator checklist:

[ ] Pull last 90 days of revenue — calculate average daily sales

[ ] Estimate repayment at 10% of revenue/day over 6–9 months

[ ] Stress-test: what if sales drop 30%? Can you cover COGs + RBF draw?

[ ] Compare 3 RBF platforms (rates + speed)

[ ] Negotiate the revenue percentage — it's not always fixed

Mini-Framework: The RBF Go/No-Go Decision Tree

Is your CAC < 30-day LTV? → Yes = proceed. No = fix economics first.

Can you deploy capital in <30 days? → Yes = RBF works. No = you'll waste fees.

Do you have 90+ days runway without the loan? → Yes = safe. No = too risky.

Pass all three? RBF is your play.

Play 3: Merchant Cash Advance (MCA) — The Emergency Rip Cord

What it is:

A lender buys your future receivables at a discount. You get cash now; they pull daily/weekly ACH debits until paid. Fast, expensive, last-resort.

When it works best:

You need cash in 24–48 hours

Banks said no

Credit score is under 600

Short-term inventory crunch or ad opportunity

Common pitfalls:

MCAs are the most expensive option — effective APRs can hit 40–80%. Daily debits wreck cash flow if sales don't spike. Stacking multiple MCAs = death spiral.

What you need to qualify:

$5K+ monthly revenue (some go lower)

Business bank account with 3+ months history

Pulse. Seriously — approval is fast and loose.

Operator checklist:

[ ] Only use if ROI is immediate and certain (proven product restock, not a gamble)

[ ] Calculate total payback — if it's >1.4x, walk away

[ ] Set a 60-day payoff plan — do NOT let this drag

[ ] Firewall MCA funds — separate account, separate use case

[ ] Never stack a second MCA on top of the first

Survival rule:

Treat MCA like a payday loan. Get in, deploy, get out.

Play 4: Inventory Financing — The SKU-Specific Play

What it is:

Lenders fund inventory purchases directly. They own the stock until you sell it, then you repay from sales. Often tied to suppliers or platforms (Kickfurther, Wayflyer, 8fig).

When it works best:

You have proven SKUs with predictable sell-through

Long lead times from suppliers (60–90 days)

You're pre-ordering for holiday or seasonal spike

You don't want to burn operating cash on COGs

Common pitfalls:

If inventory sits, you're paying holding costs or fees. And if the SKU flops, you're stuck with debt on dead stock.

What you need to qualify:

SKU-level sales data (30–90 days)

Purchase orders or supplier invoices

Wix store analytics showing conversion + velocity

Sometimes a personal guarantee

Operator checklist:

[ ] Identify top 3 SKUs by revenue + margin

[ ] Pull days-to-sell for each — anything >45 days is risky

[ ] Get quotes from 2+ inventory lenders

[ ] Negotiate supplier payment terms first (net-30 vs net-60 changes everything)

[ ] Track funded SKU performance weekly in a separate P&L

3-Step Inventory Funding Plan:

Audit velocity — rank SKUs by sell-through rate

Fund only A-players — top 20% of SKUs that move in <30 days

Set a kill switch — if a funded SKU doesn't move in 21 days, discount hard or return

Play 5: The Hybrid Stack — Layering Funding Like a Pro

What it is:

Combine 2–3 funding sources strategically. Example: Wix Capital for baseline inventory + RBF for ad spend + net-30 supplier terms.

When it works best:

You're scaling fast (30%+ MoM growth)

You have multiple cash needs (inventory, ads, payroll)

You can manage repayment calendars without losing your mind

Common pitfalls:

Over-leverage. If you stack too many debits, one bad month cascades into default across multiple lenders. Also: some lenders prohibit stacking in their terms.

What you need to qualify:

Strong financial discipline (you need a 13-week cash flow model)

Clean books

Experience managing multiple funding sources

Revenue >$50K/month (you need scale to justify complexity)

Operator checklist:

[ ] Build a repayment calendar — map every debit by date + amount

[ ] Cap total monthly outflows at 40% of revenue

[ ] Read every contract — flag "no stacking" clauses

[ ] Set a cash floor — never let operating account drop below $10K

[ ] Review stack weekly — kill underperforming channels fast

The Stack Priority Framework:

First layer: Supplier terms (cheapest capital)

Second layer: Wix Capital or inventory financing (tied to specific use)

Third layer: RBF for growth plays (ads, new SKUs)

Never: MCA unless it's life or death

Funding Options Comparison

Option | Best For | Speed | Cost Range | Requirements | Biggest Risk |

Existing Wix stores with steady sales | 24–48 hours | Low–Mid (tied to revenue) | Active Wix store, minimum sales history | Limited availability; not all stores qualify | |

Revenue-Based Financing (eg, Clearco, Wayflyer) | Scaling brands with predictable revenue | 1–3 days | Mid (6–15% flat fee) | $10K+ monthly revenue, connected financials | Repayment eats into margin during slow months |

Quick cash for inventory or ads, last resort | Same day–24 hours | High (factor rates 1.2–1.5+) | Consistent card sales, often minimal docs | Daily/weekly draws crush cash flow; expensive | |

Seasonal cash needs, controlled drawdowns | 3–7 days | Low–Mid (interest only on what you use) | Good credit, 6+ months in business | Variable rates; requires discipline | |

Bulk orders, pre-season stock-ups | 5–10 days | Mid (collateralized loans) | Purchase orders, supplier invoices | Inventory sits = loan still owed | |

Personal Credit Cards / 0% APR Offers | Bootstrappers with strong personal credit | Instant (if approved) | Low (if paid within promo period) | 700+ credit score, responsible use | Mixing personal/business finances; high rates after promo |

FAQs: Wix Seller Financing

Can Wix sellers get financing for their online store?

Yes. Wix sellers can access financing through Wix Capital (if eligible), revenue-based financing providers, merchant cash advances, and traditional business loans. Wix Capital integrates directly with your store dashboard and offers funding based on your sales history.

What is Wix Capital and how does it work?

Wix Capital is Wix's built-in financing tool that offers cash advances to eligible store owners. It analyzes your sales data and repays itself automatically by taking a small percentage of each transaction until the advance plus a fixed fee is repaid.

How much funding can I get with Wix seller financing?

Funding amounts vary by provider. Wix Capital typically offers $500–$100,000 based on your sales volume. Revenue-based financing and merchant cash advances can range from $5,000 to $500,000+ depending on your monthly revenue and business performance.

Do I need good credit to qualify for Wix store funding?

Not always. Wix Capital and revenue-based financing focus primarily on your store's sales performance rather than personal credit scores. Traditional business loans typically require credit scores of 600+, but merchant cash advances often approve sellers with scores as low as 500.

How fast can I get funded as a Wix seller?

Wix Capital decisions happen within minutes if you're pre-qualified in your dashboard. Revenue-based financing and merchant cash advances typically fund within 24-72 hours. Traditional business loans may take 1-2 weeks.

What can I use Wix seller financing for?

You can use the funds for inventory purchases, paid advertising, product photography, hiring contractors, upgrading your store design, purchasing equipment, or covering seasonal cash flow gaps.

Is Wix Capital better than a merchant cash advance?

Wix Capital often has lower fees and more transparent terms than traditional merchant cash advances. However, availability depends on your sales history with Wix. If you're not eligible for Wix Capital, a revenue-based loan or MCA from a third-party provider may be your best alternative.

What are the downsides of revenue-based financing for Wix stores?

Revenue-based financing takes a percentage of daily or weekly sales, which can strain cash flow during slow periods. The effective APR can be higher than traditional loans, and frequent remittances may complicate accounting.

Can I get Wix seller financing if my store is new?

Wix Capital typically requires at least 3-6 months of sales history. New stores may qualify for small merchant cash advances, business credit cards, or microloans instead. Building consistent revenue for several months improves your eligibility.

How do I apply for Wix Capital?

Log into your Wix dashboard and navigate to the "Business Tools" or "Finance" section. If you're eligible, you'll see pre-qualified offers. Click to review terms, select your offer amount, and submit your application—approval can happen in minutes.

Conclusion: Pick Your Poison, Then Move

Here's the truth: there's no free money. Every funding option trades something—speed for cost, flexibility for risk, convenience for control.

If you're already on Wix and moving product, start with Wix Capital. It's fast, integrated, and won't destroy your cash flow.

If you're scaling fast and need runway for ads or inventory, revenue-based financing gives you breathing room without giving up equity.

If you're desperate, a merchant cash advance will get you cash today—but it'll bleed you tomorrow. Use it only if you have a clear, short-term revenue spike coming.

The move: Pick the option that matches your current revenue, runway, and risk tolerance. Then lock it in and get back to selling.

Cash flow problems don't fix themselves. Funding is a tool. Use it smart, or it'll use you.

Next step: Apply to two options today. Compare offers. Take the one that hurts least. Then execute.

Comments